As income inequality in the United States has soared and median wages have flatlined since 1980, economists have spent a lot of time debating why the top 1 percent have done so much better than everyone else. Is policy to blame? The decline of labor? Technology?

An equally pressing question, though, is what those increasingly hefty incomes at the very top mean for the lives of everyone else. And a big, newly revised paper by the University of Chicago’s Marianne Bertrand and Adair Morse finds that there is a connection, but not a happy one: The gains of the rich have come alongside losses for the middle class.

As the wealthy have gotten wealthier, the economists find, that’s created an economic arms race in which the middle class has been spending beyond their means in order to keep up. The authors call this “trickle-down consumption.” The result? Americans are saving less, bankruptcies are becoming more common, and politicians are pushing for policies to make it easier to take on debt.

If that argument sounds familiar, it’s because Cornell economist Robert H. Frank has been making this case for years. Those at the top are spending more on fancy goods and bidding up the price of homes. In response, the slightly-less-rich have been spending more to keep pace. That pressure, in turn, eventually ripples down to the middle class — where incomes have stagnated of late — in what Frank calls “expenditure cascades.”

“What you think you need depends on the context you find yourself in,” Frank said in an interview. “And standards tend to be local. When most of the income gains are going to the very top, the people around them feel relatively poorer and spend more because of that.”

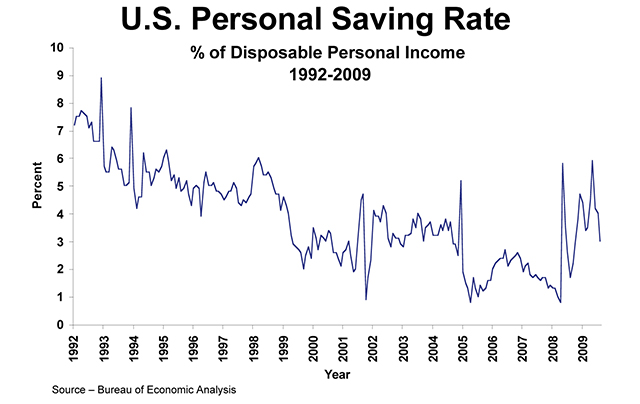

Photo: See a larger version

What Bertrand and Morse have done is put together a detailed empirical case that “trickle-down consumption” really is occurring in cities and counties around the United States — and that it’s responsible for roughly one-fourth of the decline in household savings rates since the early 1980s.

“Middle income households would have saved between 2.6 and 3.2 percent more by the mid-2000s had incomes at the top grown at the same rate as median income,” they conclude.

But how does trickle-down consumption actually work? One way is through housing. In cities like New York, the wealthiest are competing for the most valuable apartments and bidding up prices — which has broader ripple effects. What’s more, as those at the top buy bigger and bigger houses, those below them have moved to buy up bigger houses too. (Frank has noted that the median size of a new single-family house in 2007 was 2,300 square feet, or 50 percent bigger than in 1970.)

That’s just part of the story, though. In areas where incomes of the top 10 percent are growing, Bertrand and Morse found, the supply of businesses and services that cater to the well-off also increase. Swankier bars replace cheaper bars. Expensive restaurants replace cheap restaurants. Whole Foods nudges out the local grocery store. And less-well-off residents end up spending more at these places.

There also seems to be a “keeping up with the Joneses” effect. As wealthier Americans spend more on things like expensive preschools or fitness clubs or even fashion, their middle-income neighbors start spending more on these goods too — without cutting back elsewhere.

On its face, that doesn’t sound so terrible. But “trickle-down consumption” can have less-happy side effects too. In an earlier paper, Frank, Adam Seth Levine, and Oege Dijk found that “expenditure cascades” tend to lead to more bankruptcies,

higher divorce rates, and longer commutes. Keeping up with the Joneses takes a toll.

Bertrand and Morse assemble their own evidence on this. Middle-class households that are exposed to growing inequality, they find, appear to report more signs of financial distress. And, at the state level, higher inequality seems to be predictive of personal bankruptcy filings.

There are also signs — albeit tentative — that growing inequality at the top end is affecting politics in unexpected ways. The two economists find that members of Congress in districts with higher levels of income inequality were more likely to vote for a 1992 bill that greatly expanded credit for housing. That was true even after controlling for ideology.

In an interview, Bertrand said it was still unclear why this is. One possibility is that in areas with high top-end inequality, politicians are more likely to favor policies that allow middle-class Americans to borrow more so that they can keep up. Another possibility, though, is that high inequality at the top is driven by a growing financial sector — and so politicians are more willing to loosen credit to placate the banks.

Either way, this dynamic can be harmful to economic growth over the long run, as a 2011 report from the International Monetary Fund found (see chart). When inequality runs rampant, the IMF argued, people on the lower end tend to borrow more to keep afloat. That excess debt, in turn, increases the risk of a major financial crisis. This new paper adds a bit more detail on how these situations can develop.

For her part, Bertrand argues that the effects of inequality on the political system could use more research. “Academics spend a lot of time looking at the causes of rising income inequality,” she says. “But surprisingly, there’s much less work on the consequences.”

3 WAYS TO SHOW YOUR SUPPORT

- Log in to post comments