GREENVILLE, Miss. — Linda White misses the Greenville that she knew. When she was a little girl, her Mississippi Delta hometown was filled with shops, factories and people. But recent decades have changed all of that.

“If you go down Washington Avenue, you would think that the town is deserted,” she said. “The people that were here that long ago are gone.”

Over the years, factory after factory along the Mississippi River went down, with the recession dealing the final blow, she said. As other businesses moved out, it became harder for residents of this town — dubbed the heart and soul of the Delta — to take care of some basic needs.

After the recession began, high-profile bank failures grabbed headlines, but another effect of the economic collapse has had a more direct impact here and in communities around the country.

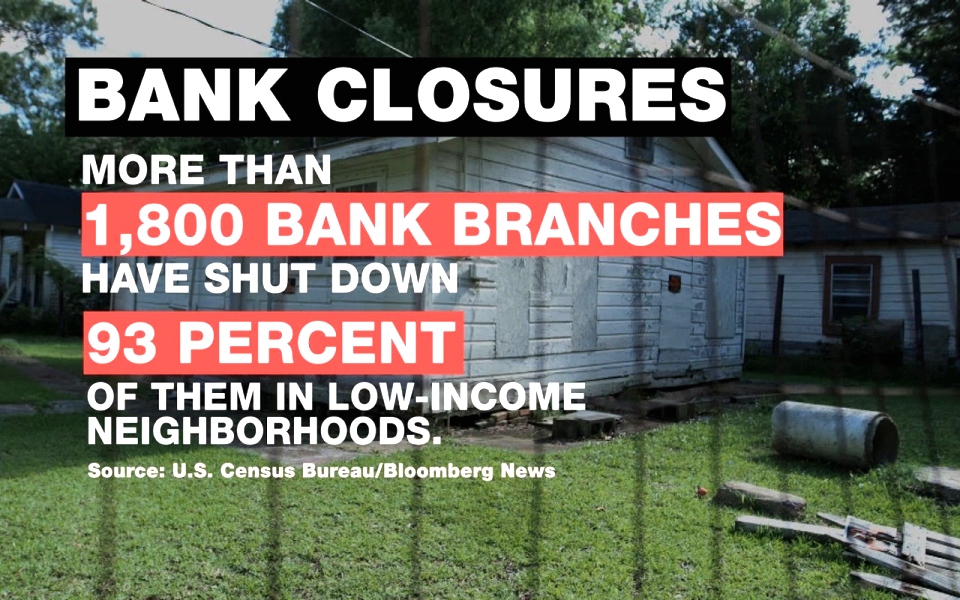

Between 2008 and May 2013, more than 1,800 bank branches shut down nationwide — 93 percent of them in low-income neighborhoods, according to Bloomberg. More than one-fourth of all U.S. households are “underbanked” — forced to rely on alternative services like payday lenders, according to the Federal Deposit Insurance Corp.

Living in an “unbanked” or “underbanked” area can be extremely expensive. Many people rely on pawnshops or payday lenders for banking tasks like paying bills and cashing checks, which can trap them in a cycle of serious debt.

Overall, more than 68 million Americans live in “bank deserts” — defined by the U.S. Postal Service as communities with one bank or fewer. In 2012 alone, these Americans spent $89 billion on interest and fees, an average of $2,412 per underserved household, for alternative financial services. It’s a market that the financially embattled USPS has considered entering.

When people living check to check rely on pawnshops and payday lenders to make ends meet, the real cost is written in the fine print.

“While many of our residents don't want to use … these places, they will because it's convenient,” said Kimberly Hilliard, who specializes in urban planning at Jackson State University. “But many of us cannot afford to inherit the fees … When you go outside of a traditional bank and you go to a payday lending [service], the fees that you incur will be quite significant, and many of our families cannot afford it.”

In the Mississippi Delta, the number of residents lacking access to basic financial services is now more than twice the national rate. For White, a working mother of three, that meant fewer options to help buy her first home.

Having worked for 20 to 25 years, she wanted to own a home. But she said the bank told her she couldn’t afford a mortgage.

“It was very frustrating,” said White. “I wasn't destitute. I had money, and I had been a member of a bank over 10 years. I mean, when you put your money in a bank over 10 years, you expect them to at least give you a loan for a home that you really need, and you know they will get their money back. But they never did.”

When Banks Bail

Mississippi residents face an especially difficult financial battle. The Magnolia State ranks worst in poverty, and nearly one in five households lacks a relationship with a traditional financial institution.

Hilliard said some older neighborhoods suffer “complete disinvestment.”

“We call it the broken window syndrome, where there's a broken window because someone moved out,” she said. “Then you have abandoned dogs running around. Then you have overgrown weeds, and you can just see the life of the neighborhood being zapped out. And people who have choices will move out. But people who have the least amount of choices will stay.”

Bill Bynum, CEO of Jackson-based Hope Federal Credit Union, is working to fill the void being left by big banks.

“The largest banks in the country and in the region have shut down branches — not because those communities weren't viable or the branches weren't profitable, but they weren't profitable enough for their business model,” he said.

Hope, a financial cooperative owned and managed by customers, opened in 1994 in a church basement with a mission to improve lives in the nation's most depressed region.

“We think those people and places are important,” said Bynum. “We've been able to go in and structure financial services to meet the needs and stabilize those communities.”

With 30,000 members and $200 million in assets, Hope is working to bring financial options to people across the mid-South.

“It's hard to avoid the connection between race and poverty,” Bynum said. “And as the country becomes more diverse, it's even more important that we take steps to try to address those issues. And we believe that access to capital, access to financial services, is an important piece of the puzzle.”

According to the Urban Institute, white Americans had an average of six times the wealth — measured by savings, real estate and retirement accounts minus debts — of blacks in 2010.

“Mississippi, Arkansas, Louisiana, Tennessee — the states where we work in — have a quarter of the [most] persistently impoverished counties in the country,” Bynum said. “It's those counties that have had 20 percent poverty for at least three decades in a row. A quarter of those counties are here in the mid-southwestern-most parts, the Black Belt.”

In Over Her Head

As with so many Americans struggling with debt, Gloria Warner’s financial trouble started with a single transaction.

“It started out being with the car problems,” said the native of Jackson, Mississippi. “And then I went to one payday loan, and I had to get money there. Then I had to go to another payday loan to keep up with the payment from the first payday loan. Then I end up having problems with the house because the house I stay in is a family home as well, and we're trying to refi. So I had to come for that. And it's just a cycle that kept going and going and going.”

Warner ended up $2,800 in the hole.

“It got so bad,” she said. “I felt I was working for the payday loan instead of working to try to pay bills because it was, like, I had to pay payday loans first and then pay my bills.”

In a four-year span, Warner juggled eight different loans from eight different payday lenders.

Many other Americans find themselves in a similar situation. Every year, 12 million Americans do business with payday lenders, taking an average of nine different high-interest loans, according to the Center for Responsible Lending.

“I came in one day, and I looked at my check. And I went head on,” she said. “After I did the payday loans, I couldn't even go really buy groceries for my house.”

At the end of the day, just $20 was left of her check.

She turned to Hope for help, and has since paid off her payday loan debt.

“I think if Hope wouldn't have came in, I'll still be doing that same ritual thing,” she said. “And even though they say they offer you a way out, I just couldn't see it.”

"Hope Was My Last Hope"

One hundred miles south of Greenville sits the sleepy town of Utica, Mississippi, which shares a similar economic story from recent decades.

“When I first came to Utica, Utica was a hustle-and-bustle little town,” former Mayor Jesse Killingsworth said. “We had dentists. We had hardware stores. We had doctors’ offices. A lot of things have changed, really.”

But along with medical offices and stores, the bank for the town of 850 shut down.

“When BancorpSouth, which was the existing bank for quite a few years, made a corporate decision to leave, the town was in total disarray,” Killingsworth said. “We really didn't know what we were going to do without having to travel over 30 or 40 or 50 miles to a financial institution.”

Hope Federal Credit Union stepped in.

“I like to make a comparison: Just like fertilizer is to the farmer to make the plants grow, a financial institution does the same thing for the community,” Killingsworth said. “It provides the grease that keeps the community together and keeps it a well-oiled machine.”

Killingsworth said Hope’s model is working.

“When I first started talking to Mr. Bynum about Hope, I said, ‘A credit union actually belongs to its members,’” he said. “So I feel like I'm vested in the credit union. It's the people's bank. The people of Utica.”

Back in Greenville, White got the financing to move into her dream home after a decade of waiting.

“Hope was my last hope,” she said.

As the economy makes an uneven recovery across America, Hope is helping other people in the mid-South stay put and stay invested in their communities.

White said she’s still hopeful about her future and her community’s.

“I'd just like to see people live the kind of life that we lived in Greenville a long time ago.”

Originally published by Al Jazeera America

3 WAYS TO SHOW YOUR SUPPORT

- Log in to post comments